Fintech - future of financial inclusion? [India]

Next Billion Tech

"We will always need banking, but we will not always need banks" ~ Bill Gates

I believe the most critical link for any sector is financial inclusion – whether student lending, farmer risk coverage, micro-entrepreneur financing options, health insurance, SME lending. If you see the current Indian or any emerging economy market, it is still so immature in terms of financial inclusion, and the adoption of services and products is extremely limited to high to middle-high income.

For the last few days, I am trying to understand the fintech or financial services space in India and other similar emerging economies like Indonesia and SEA.

What kind of products existing in the market?

What kind of innovation is happening in this space?

Who are the active investors?

What are the themes under which investments are happening?

It is in no way an investor expert opinion but solely my attempt to share my insights, derivations, and conclusions about where the industry is moving as an outsider to the industry.

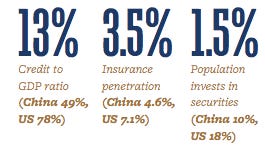

To start with, I delve deep into Kalaari's report – "Uniquely India Digital Opportunity, which I thoroughly enjoyed reading, and it helped me understand the state of the financial inclusion in India.

"Having a sizeable banked population is the first step in the direction towards financial inclusion, but India has a long way to go as far as penetration of financial products is concerned."

InsightsDespite tech in fin-tech, most of the companies in this space are an extension to existing financial institutions by adding over a layer of technology and becoming origination/front end for banks and NBFCs. I summarise this trend as the phase zero of fin-tech in India, where mostly digitization has happened with little or less disruption to existing methods.

The rapid growth in penetration of smartphones and 4G internet (thanks to Jio) has accelerated usage of e-wallets, e-commerce transactions, which has helped to leapfrog credit card infrastructure.

All transfers are data transfers – then why to maintain a physical book or ledger – Isn't banking now basically a 'data' business?

I observed most of the investors' money is floating under the following headers (this is just my observation among the companies that started between 2015-2018, which has raised money above $1 mn):

Payment gateways like Cash Free, Razorpay

e-Wallets or UPI interface like PayTM, PhonePe, MobiKwik, Freecharge, BharatPe

There are savings platforms like Groww, INDwealth, Wealthy, GoalWise, Sqrrl, Cube, Kuvera. This space is still at nascent stages in terms of product offering, as most of them are still targeting India-1 customers, who want to invest in mutual funds. All thanks to the "mutual fund Sahi hai" campaign.

There are insurance platforms like Turtlemint, Toffee, Digit Insurance, Gramcover

The last and the most crucial bucket where the investors are pretty active is lending, under the two following buckets:

MSME/SME – KNAB, Lendingkart, Indifi, FTCash, NeoGrowth, Capital Float

Unsecured credit to, e.g., salaried employees, e-commerce consumers – Paysense, LiquiLoans, Anytimeloan, MoneyOnClick, Money Tap, KrazyBee, Zest Money, SlicePay, Loan Tap, Kissht. This space is overcrowded.

After going through several business models and products, in general, what I got a sense was most of them are in the space of incremental improvement in terms of access to existing financial services and mostly offering to India-1 and 2. So, there is a huge opportunity to create customized and personalized products for India-3 and India-2, i.e., mid-income and low income.

What fin-tech companies need to figure out to disrupt (not just an incremental improvement)?

- Know the customers' ability to pay vs. willingness to pay

- To be able to determine the fraud and credit model

- Use positive screening over negative screening while creating a credit or fraud model.The smartphone is helping enable a new line of credit services:

Conclusion I would love to see ventures using alternate data models while designing savings, insurance, and lending products. The data can come from smartphones, the digital footprint of the consumers, and other behavior data point sources. E.g. , Tala, Branch, HealthIQ, which are redefining the usage of new data sets related to behavioral economics, nudges, positive/negative screening.

I am hopeful that we see disruptive, scalable, and profitable models in the fintech and insuretech industry in the coming future instead of being copy cats of each other, which I somehow feel is happening presently.

“Financial services in India is going from low volume, high value, high cost to high volume, low value, low cost” ~ Nandan Nilekani

Referenceshttps://www.omidyar.com/sites/default/files/18-11-29_Report_Credit_Disrupted_Digital_FINAL.pdf

https://www.toptal.com/finance/investment-banking-freelancer/fintech-and-banks

I am continuously looking for fin-tech solutions that can create mass-market fin-tech products for direct consumers or M/SMEs. If you are building one or investing in one in Indonesia or SEA, please do write to me, I would love to learn more from you.

With Love,

Sagar

About

"first followers" is founded by Sagar Tandon, a founding member at Moonshot Ventures. You can reach him at sagar@moonshotventures.org.

Occasionally, he blogs about the responsible investing, tech for good, venture capital, investment thesis, conscious capitalism, collaborative consumption, community, and humane lifestyle.